The bulk of existing research places financial investment at the forefront of price determination for gold but while the short-term impact of financial markets is undeniable, the long-term importance of other sources of buying is even more so.

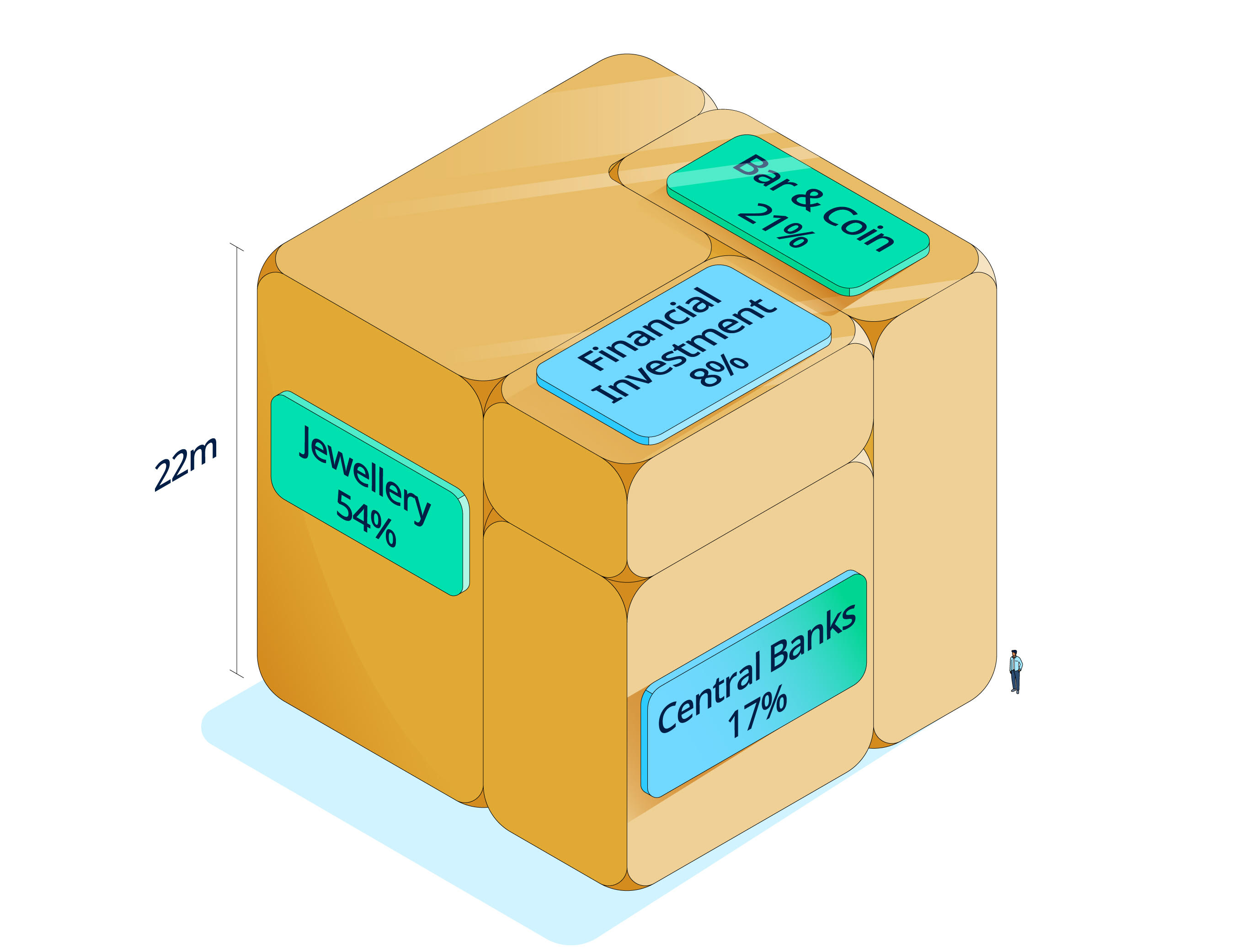

The estimated above-ground stock of gold, at 212,582 tonnes, which we depict as a cube, is a balance sheet snapshot of gold ownership (Figure 2). It is remarkable for a number of reasons.

The cube illustrates how the total stock of this ubiquitous metal could occupy a physical space barely larger than three Olympic-sized swimming pools. In addition, it reveals how little financial investment – (referring here to physically backed gold ETFs and over-the-counter (OTC) physical holdings) has been amassed by market participants over the years in relation to other sources of demand – a misleading statistic given the vast volumes of gold that flow through financial centres every day.

That so much of this hypothetical cube is not owned via financial instruments implies that any explanation of its total distribution must consider factors beyond those solely linked to the day-to-day decisions of financial market participants.

The distribution of the cube also suggests that the price of gold has been driven by two distinct components: an economic component combined with a financial component.

Figure 2: The cube of above-ground gold stocks shows gold’s ownership across sectors of demand

Estimated above-ground gold holdings by category*

*Data as of Q1 2024. Financial investment includes OTC and gold ETF. Source: World Gold Council, Metals Focus, Refinitiv GFMS

We illustrate an example of these dynamics in Chart 1 using quarterly data from 2000, adding COMEX futures net positions to the mix to capture derivatives activity.1 This compares the cumulative net consumer flows (jewellery plus technology minus recycling) to flows relating to gold financial instruments (gold ETFs, plus OTC net buying and net long futures positions). The volume from gold accumulated through financial instruments is more than twice as volatile as net consumption, yet accumulates at a much lower rate.

It is this accumulation – whether for individuals, the reserves of select central banks or even investment for long-term savings – that we attribute to an economic component. The financial component represents, more tactical considerations, such as hedging demand, whether from individual or institutional investors.2

These components closely match the drivers we have outlined in our other pricing models, GRAM and Qaurum. Additional drivers, including risk and uncertainty and momentum are less relevant in the long run but feature heavily in the short run (see Focus 1).

Chart 1: Financial investment is more volatile and accumulates more slowly than consumer and retail bar and coin demand

Cumulative gold demand since 2000 across categories*

*Data as of Q4 2023. Consumption represents jewellery and technology less recycling. Retail bar and coin follows our standard definition as reflected in Supply and demand notes and definitions. Financial investment and futures captures OTC, ETF and COMEX futures demand. Source: Bloomberg, Metals Focus, Refinitiv GFMS, World Gold Council

The cube illustrates how the total stock of gold could occupy a physical space barely larger than three Olympic sized swimming pools.

Focus 1: Gold's key drivers

Gold’s performance responds to the interaction of its roles as a consumer good and as an investment asset. It draws not only from investment flows but also from fabrication and central bank demand.

In this context, we focus on four key drivers to understand its behaviour across periods:

Economic expansion: periods of growth are supportive of jewellery, technology and long-term savings

Risk and uncertainty: market downturns, inflation and geopolitical risk often boost investment demand for gold as a safe haven

Opportunity cost: the price of competing assets, including bonds and currencies, influences investor attitudes towards gold

Momentum: capital flows, positioning and price trends can boost or dampen gold’s performance.

Although COMEX futures ownership, and indeed that on other futures exchanges, does not explicitly exist in the cube, eligible and registered stocks do, and some positions in the futures market are hedged using physical gold. More importantly, we add futures to the mix as they play an important role in price discovery in the short term and add to short-term turnover in markets.

The dual nature of gold drivers was covered extensively by Goldman Sachs as part of its Fear and Wealth framework; see Appendix D for our analysis. In addition, the model developed by Barsky et al. (2021) employs real GDP as a significant driving factor behind the price.

Diversification does not guarantee any investment returns and does not eliminate the risk of loss. Past performance is not necessarily indicative of future results. The resulting performance of any investment outcomes that can be generated through allocation to gold are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. The World Gold Council and its affiliates do not guarantee or warranty any calculations and models used in any hypothetical portfolios or any outcomes resulting from any such use. Investors should discuss their individual circumstances with their appropriate investment professionals before making any decision regarding any Services or investments. This information may contain forward-looking statements, such as statements which use the words “believes”, “expects”, “may”, or “suggests”, or similar terminology, which are based on current expectations and are subject to change. Forward-looking statements involve a number of risks and uncertainties. There can be no assurance that any forward-looking statements will be achieved. World Gold Council and its affiliates assume no responsibility for updating any forward-looking statements.

Information regarding QaurumSM and the Gold Valuation Framework

Note that the resulting performance of various investment outcomes that can be generated through use of Qaurum, the Gold Valuation Framework and other information are hypothetical in nature, may not reflect actual investment results and are not guarantees of future results. Neither World Gold Council (including its affiliates) nor Oxford Economics provides any warranty or guarantee regarding the functionality of the tool, including without limitation any projections, estimates or calculations.